The Operating Environment Assessment Paper - June 2023

INC’s win in Karnataka does not signal that the BJP should worry too much about 2024 – but a new opposition grouping could emerge from it

Congress’ resounding victory in the Karnataka Assembly election may have, however slightly, straightened the pitch ahead of 2024. Its success owed to a focused, tightly-run campaign, as well as a collapse in support for the JD(S), which helped consolidate the anti-BJP vote. Although the BJP managed to retain its ~36% vote share in the face of strong anti-incumbency pressure, its base was more regionally concentrated than 5 years ago, signalling some erosion in its broader appeal. The result also highlighted, yet again, that the BJP is more beatable in a two-way than in a multi-pronged fight. This has triggered renewed interest among opposition parties to build a combined front that can take on the frontrunner. Whether they can successfully negotiate seat-by-seat allocations, as well as a common manifesto, without descending into chaos, remains to be seen. However, such a front now seems plausible – which it decidedly was not a few months ago. Interestingly, even Congress’ fractured Rajasthan unit is presenting a united front for the upcoming state election.

The Budget session was unproductive but the Monsoon session promises discourse on some key bills

Various wings of government have recently approved key policies

On the policy front, following a lacklustre Budget Session, there are now 37 bills pending approval before Parliament. Current indications are that the Digital Personal Data Protection Bill will find passage during the Monsoon Session alongside the Telecom and Electricity (Amendment) bills. Other important laws that may get discussed or even move forward include the DESH Bill, which seeks to replace the current SEZ Act, and a Repealing and Amending Bill. Outside of the Central legislature, the Cabinet approved a new Space Policy that introduces a revamped regulatory framework for the sector and establishes IN-SPACe as an independent agency to foster the industry’s growth with ISRO's assistance. The Cabinet also approved a new PLI scheme for IT hardware worth Rs 170 billion, with the potential to generate additional investment of Rs 243 billion and 75,000 jobs. The upcoming Foreign Trade Policy is expected to designate a number of towns as having potential for export excellence; bring revisions to the Export Promotion Capital Goods Scheme; and launch new initiatives to promote e-Commerce exports, such as enabling access for international vendors to international markets.

A flurry of foreign trips by Mr Modi is deepening India’s engagement with its major partners

Prime Minister Modi’s recent visit to Japan for the G7 summit showcased India’s deepening leadership in the Indo-Pacific region. Significantly, too, India played a leading role in a separate Japan-led conference seeking to enhance cooperation among countries of the Global South, including on issues such as food security. This is being seen as a direct response to China’s rising assertiveness on regional issues. The fifth Quad Summit, held alongside the G7 meetings, reaffirmed the commitment of the member countries to the grouping, while Mr Modi's meeting with Ukrainian President Zelensky emphasised India’s neutral stance on the war – crucial at this stage, when India holds the G20 presidency. Looking ahead, the PM’s state visit later this month to America will may send a strong message on the growing geopolitical and economic alignment between India and the US. The trip is expected to boost defence and trade cooperation, with an influx of fresh investments from US companies as part of their diversification strategy away from China.

A Macroeconomic Review

GDP growth was much stronger than expected in Q4, taking FY23 growth to 7.2%

At 6.1%, India’s Q4 (Jan-Mar) GDP growth was much stronger than expected, though it came on the back of a low 4% base from last year. Resultantly, full-year FY23 growth came to 7.2% - well below last year’s low-base-driven 9.1% but slightly higher than the official (7%) projections. For FY24, the IMF (5.9%, down from an earlier 6.1% forecast) and most private agencies have pegged growth at or below 6%, primarily on account of external weaknesses and tight money, which is crimping private expenditure. However, with inflationary pressures easing, and given the carry-over of strong growth momentum, there may be room for some upside (~25-50 bps) to these forecasts.

Growth has been strong across sectors, and is plainly normalising

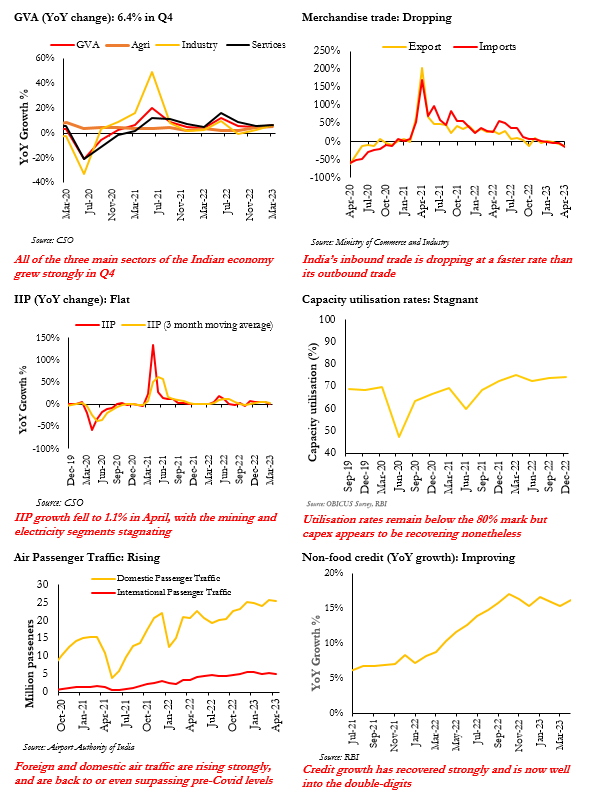

Q4 growth was robust across the 3 main sectors of the economy, while for the year as a whole, only manufacturing remained below trend. Services expanded by 9.5% in FY23, shaking off any lingering weakness from the pandemic years. The trade, hotels, transport and communication services segment grew by 14%, up from 11.8% the previous year. Financial, real estate and professional services saw a 7.1% rise, up from 4.7%. However, public administration, defence and other services – a proxy for the government’s non-capex spending – decelerated from 9.7% to 7.2% as the state reined in its accommodative fiscal policy. The manufacturing sector grew by 4.5% in Q4 following two consecutive quarters of contraction. Still, owing to a heavy base effect (FY22 growth was 11.1%), full-year growth was just 1.3%. In FY24, as this factor wears off, the headline figures should be a more ‘normal’ 4.5-5%. On the other hand, construction activity remains strong, expanding by 10% even on a high, 14.8% base.

Agricultural output growth is steady but El Niño poses risks to farm yields

Agriculture grew by an unexpectedly fast 5.5% in Q4, the quickest in three years, taking annualised growth to 4%, up from 3.5% in FY22. However, with an El Niño pattern developing over the South Pacific, there is a dark shadow over this year’s monsoon. Even as the Indian Meteorological Department (IMD) continues to project ‘normal’ rainfall, Skymet, a reliable private weather forecaster, has pegged it as ‘below-normal,’ with a 60% chance of drought. (Over 2001-2020 period, there were 7 El Niño years, of which 4 resulted in droughts.) Even if aggregate rainfall does turn out to be normal, these conditions may create extreme variability in the spatial/temporal distribution of rainfall, particularly in the second half of the June-September season. North India is especially likely to see below-normal rainfall. Even as crop diversification and the spread of irrigation have made India less rainfall-dependent than before, a poor summer crop would certainly impact rural incomes and thus demand.

Lead indicators look strong…

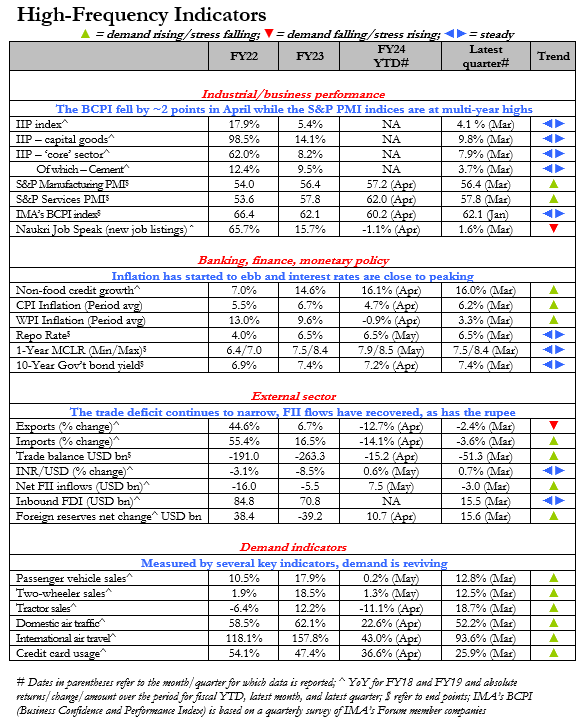

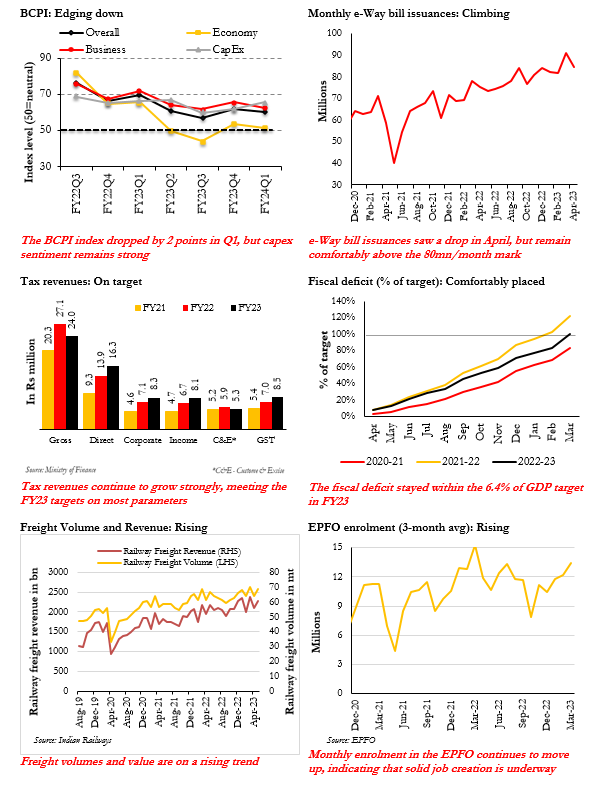

Judging by the lead indicators of growth, the strong momentum seen in the last few months of FY23 has continued in the new year. Monthly GST receipts stayed above the Rs 1.4 trillion mark through FY23 and have continued to move up. They briefly dipped to Rs 1.57 trillion in May from April’s record Rs 1.87 trillion, but should recover in June, with e-Way bill issuances jumping to 88 million from 84 million the previous month. Non-food credit growth has also steadily accelerated, averaging 10.3% last year, but was a robust 16.1% in April, with credit to the services sector expanding by 21.6%. The closely-watched S&P Purchasing Managers Index (PMI) touched a 13-year-high of 62 in April before easing slightly to 61.2 in May. The Manufacturing PMI rose from 57.2 in April to 58.7 in May, its highest level since October 2020. Meanwhile, IMA’s quarterly BCPI (Business Confidence and Performance Index) saw a slight decline from 62.1 in January to 60.2 in March but remained comfortably in the expansionary zone. (Values above 50 indicate net optimism while levels above 60 are indicative of moderately strong but not exuberant growth).

…and the investment cycle is reviving

Led by huge public infrastructure spending – budgeted at Rs 10 trillion this year – the capex cycle also appears to be turning. In FY23, gross fixed capital formation (GFCF) rose to 34% of GDP, up 1.3 pp from FY22. GFCE also hit a recent quarterly high of 35.3% in Q4. The BCPI data mirrors these trends, with a growing majority of respondents – 70% in the April survey – reporting that they plan to put money on the ground. Finally, automotive sales rose by a solid 21% in FY23, with all segments on an upward trajectory: 17.9% for passenger vehicles, 18.5% for two-wheelers and 38.3% for commercial vehicles. As in most years, April saw tepid/negative growth across most segments of auto, but growth resumed in May – at 9.3%, 4.3% and 7.2% for 2-wheelers, PVs and CVs, respectively.

Indicators and forecasts at a glance |

| FY21 | FY22 | FY23 | FY24* |

Economic growth (%, 2011-12 prices) |

GDP | -5.8 | 9.1 | 7.2 | 6.0-6.5 |

Agriculture^ | 4.1 | 3.5 | 4.0 | 2.8-3.2 |

Manufacturing^ | 2.9 | 11.1 | 1.3 | 4.5-5.0 |

Services ^ | -8.2 | 8.8 | 9.5 | 7.0-8.0 |

Inflation |

CPI (%, average) | 6.2 | 5.5 | 6.7 | 5.0-5.5 |

WPI (%, average) | 1.3 | 13.0 | 9.6 | 3.5-4.0 |

Public finance |

Government borrowings, Rs tr | 18.2 | 15.8 | 14.2 | 17.9** |

Receipts net of borrowings, Rs tr | 16.9 | 22.1 | 27.6 | 27.2** |

Expenditure, Rs tr | 35.1 | 37.9 | 41.8 | 45.0** |

Fiscal deficit (% of GDP) | 9.2 | 6.7 | 6.4 | 5.9** |

External sector |

INR/USD (end of period) | 73.5 | 75.8 | 82.2 | 83.0-85.0 |

Trade deficit USD bn | 161.4 | 100.1 | 263.6 | 250-270 |

Current account balance (% of GDP) | (-) 0.9 | (-) 0.9 | (-) 2.2-2.3* | (-) 1.5-1.8 |

*IMA India forecasts unless otherwise indicated; **Government estimates; ^ GVA at basic prices (2011-12 base) |

Source: CSO, RBI, DGCI&S, Ministry of Finance and CEIC. |

Consumer demand poses big questions

One big question mark around growth in FY24 concerns consumption, which has historically powered the economy. At 58.5% of GDP (a marginal, 20 bps rise over FY22), private final consumption expenditure (PFCE) was guarded in FY23. Worryingly, having shown promise in the first 3 quarters, peaking at 61.3% of GDP, it slumped to 55% in Q4. This seems to confirm the view emerging from our recent discussions with forum members from various segments. Weighed down by rising prices and uncertainties about the economy, consumers are spending only in some pockets. Apparel retailers report either falling footfalls in their stores or lower realisations, with the average customer picking up perhaps half as many items per visit as a year ago. FMCG firms are seeing decent top-line growth, but this is being driven by rising prices rather than volumes, which are flat. Conversely, official data indicate a spike in the import of luxury products such as preserved oils and high-value cheese (up 24-33% in Apr-Jan) and alcohol (up 54%). Domestic and international air traffic is surging, while theatre chain PVR reported Q4 revenues that were over twice last year’s levels. Consumption is plainly now multi-track, but most agree that pent-up demand has eased and ‘revenge shopping’ has mostly run its course. Currently, on average, forecasters are pencilling in a slightly lower rate of growth for PFCE (5.8%) than GDP growth (6%).

Inflationary pressures are easing off

More positively, inflationary pressures are likely to continue easing in the months ahead. Last year, retail (CPI) inflation averaged 6.7% and wholesale (WPI) inflation 9.6%. However, the headline numbers appear to have peaked, and in April, CPI inflation fell to a 16-month low of 4.7% while WPI inflation was at -0.92%. The key driving factors were a waning base effect, the combined impact of the RBI’s recent rate hikes, a normalisation of commodity and other input prices, the rupee’s recent stability and an overall tempering of global inflation, together resulting in lower ‘imported inflation’. The RBI is currently projecting CPI inflation to average 5.1% in FY24 – and its bi-monthly household surveys reveal that inflationary expectations have fallen from the low double digits to high single digits. The main short-term risk factor is a below-par monsoon, which could lead to a spike in food prices. While the RBI has kept the Repo rate at 6.5% for two successive MPC meetings, depending on the future trajectory of inflation, it may affect cuts amounting to 25-50 bps later this year. This should provide a mild stimulus in the second half.

External conditions have improved even as slow merchandise trade will dampen growth in manufacturing

Another welcome trend is a gradual ebbing of external pressures. Following a stellar FY22, Indian merchandise exports rose by a modest 6.7% and imports by 16.5% last year, causing the trade deficit to balloon to USD 263 billion. However, trade flows have slowed or even turned negative in recent months, with April seeing declines of 12.7% and 14%, respectively, in exports and imports. This, though, allowed the deficit to narrow sharply, and in April, it fell to its lowest in 21 months. (In FY24, merchandise exports, particularly to China and the EU, may slow further, exerting stress on exporters, many of whom belong to the SME segment that is so crucial to job creation.) At the same time, services exports – primarily IT and ITeS – surged by 42% last year, to USD 323 billion, according to preliminary data from the Commerce Ministry. Spending on software and IT services is expected to keep growing and may touch USD 400 billion this year. Private remittances have also picked up sharply. Resultantly, the current account deficit (CAD), which was projected in mid-year to exceed 3% of GDP, has narrowed rapidly. It fell from 2.8% in Q1 and 3.7% in Q2 to 2.2% in Q3. Cumulatively, it was 2.7% in Apr-Dec, well above the year-ago figure of 1.1%, but once the Q4 numbers come in, the FY23 total should end up in the 2.2-2.3% range. In FY24, it should narrow further, to 1.5-1.8%.

FII flows have revived, stabilising the rupee and local markets, but FDI receded last year

Financial and currency markets have gradually stabilised in recent months as global risks recede, inflation ebbs and central banks near the peak of their tightening cycles. India has been a key beneficiary. On net, FIIs withdrew USD 5.5 billion from India in FY23, which was an ‘improvement’ over the USD 16 billion that left in FY22. However, in April and May, they put in USD 7.5 billion, roughly three-fourths of which came just in May. Consequently, financial markets have recovered, the rupee’s depreciation has slowed or partly reversed, and a sense of optimism has returned. Eventually, this may translate into consumer spending via the wealth effect. Direct investments are a different story. Last year, gross FDI fell at its steepest rate in a decade, declining by 16% to USD 71 billion. Net FDI, which accounts for reinvested earnings, fell by an even-larger 27% to USD 28 billion, as a result of falling gross inflows and increased repatriation. However, it is likely that the situation will improve this year, primarily owing to the same global factors as above, but also thanks to India’s status as probably the world’s fastest-growing major economy.