Thursday September 14, 2023

Operating Environment Assessment Paper - September 2023

Alliances are firming up ahead of the 2024 (or late 2023) polls

As the next general elections approach, India’s political landscape is rapidly changing. The formation of the INDIA bloc of opposition parties, which seemed a distant dream only a few months ago, is now a reality. In response, the BJP is bolstering its own alliances, including ones with smaller regional parties that may not yield more than a single seat each. However, it remains the clear frontrunner, hoping to retain power on the strength of its performance, welfare spending and PM Narendra Modi’s undimmed popularity. In contrast, the INDIA bloc will seek to capitalise on anti-BJP sentiment, but will face challenges in defining a clear agenda and more so, in finalising tricky seat-sharing arrangements at the ground level. The very possibility of early elections being called will further throw the alliance off balance.

Regardless of what happens, December will see interesting state elections

Even in the absence of early polls, December will see intense competition between the two alliances in five states holding assembly elections. In a sense, these could also prove to be a template for 2024. On balance, Mizoram and Telangana are likely stay with the ruling regional parties, and Chhattisgarh with the Congress. In contrast, Rajasthan and Madhya Pradesh are likely to see a stiff contest between the two main national parties. In MP, the ruling BJP is facing strong anti-incumbency pressures but may pull through on the back of recent welfare spends and Mr Modi’s appeal. Rajasthan, which traditionally swings between the two parties with each electoral cycle, currently looks like a toss-up. However, much may depend on whether and how well the INDIA parties are able to coordinate their ground campaigns.

The Monsoon Session was productive, despite heated disagreements over multiple issues

A brief monsoon session of Parliament saw an unsuccessful no-confidence motion as well as the introduction of 25 bills, of which 23 were ratified. These include Digital Personal Data Protection Bill, the Electricity Amendment Bill and notably, the NCT of Delhi (Amendment) Bill, which sparked intense discussions. Additionally, three bills aimed at modernising India’s longstanding criminal laws and procedures were introduced but were sent for review to a standing committee. Outside of Parliament, important regulatory changes have recently been brought in by SEBI, which has tightened the framework around ESG ratings; and by the Ministry of Power, which unveiled a new Carbon Credit Trading Scheme, formally creating a trading framework.

The G20 was a diplomatic success for India – and the Global South

The just-concluded G-20 Summit in Delhi was a diplomatic success for India. Against expectations, Indian diplomats helped bring everyone abroad on the New Delhi Declaration, which neatly sidesteps differences over the conflict in Ukraine. This underscored India’s growing global stature and ability to partly counterbalance China’s influence. Under India's leadership, the G-20 welcomed the African Union as a full-time member and made firm commitments on critical issues like climate change and debt sustainability. It

also launched several noteworthy developments, including a Biofuels Alliance and a promising India-Middle East-Europe Economic Corridor (IMEE EC).

A Macroeconomic Review

GDP growth was marginally lower than expected at 7.8%

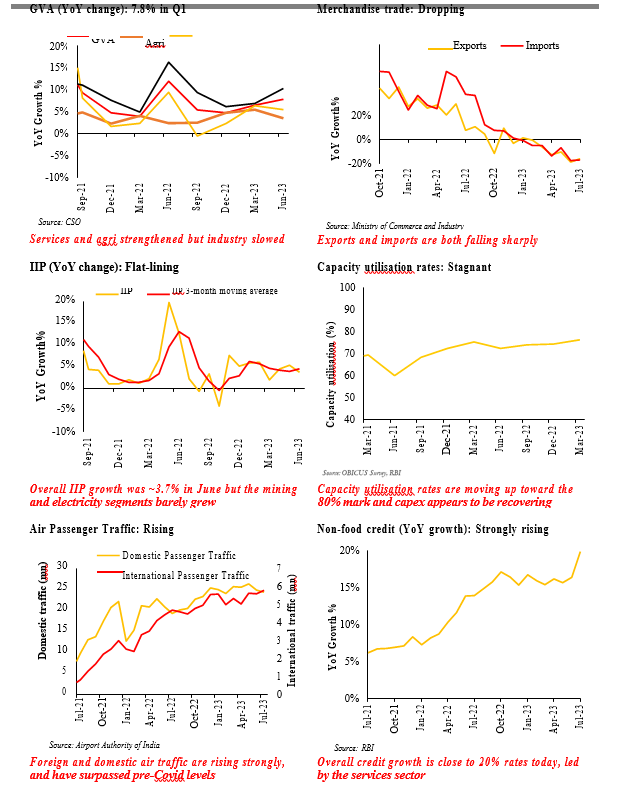

At 7.8%, India’s Q1 (Apr-June) GDP growth was strong yet marginally lower than street estimates of ~8%. What made this performance more credible was the fact that it came on a high base of 11.9% growth in the year-ago quarter. Most lead indicators remain strong, suggesting a sustained growth momentum in Q2, and the IMF recently bumped up India’s FY24 growth forecast to 6.1%, from 5.9%. However, we expect growth to taper off in the second half of the year, owing to factors such as a weak monsoon, slowing world GDP and trade growth and a revival in inflationary pressures, which will impact lending rates and hence, consumer spending, business profit margins and investment. Keeping these factors in mind, we retain our full-year growth forecast of 6-6.5%.

Services and agriculture accelerated but manufacturing slowed in Q1

Q1 growth was uneven across the 3 main sectors of the economy. Services, which constitute ~53% of GDP, expanded by 10.3%. Within services, financial, real estate and professional services accelerated from 8.5 to 12.2%, whereas the trade, hotels, transport and communication services segment decelerated to 9.2%, from an unsustainable 25.7%. Public administration, defence and other services – a proxy for the government’s non-capex spending – dipped to 7.9%, from a scorching 21.3%. The manufacturing sector slowed from 6.1% a year ago to 4.7%, but this was still its highest quarterly rate of growth since Apr-Jun 2022. Construction activity also weakened, to 7.9%, but again, this came on a high base of 16% in the year-ago quarter. Agricultural output also grew, by 3.5% (up from 2.4% a year ago), but decelerated on a QoQ basis (5.5% in the fourth quarter of FY23). More worryingly, with August seeing extended dry patches across much of India, this year’s monsoon is likely to be below normal – even if expectations of a revival in September play out. This will have a bearing on food prices, as well as rural demand, in the coming 2-3 quarters.

The lead indicators remain solid

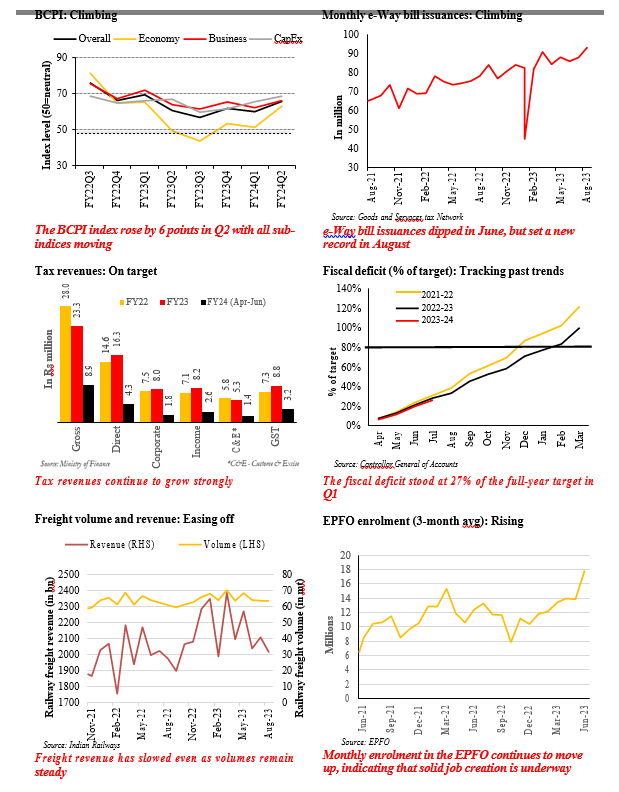

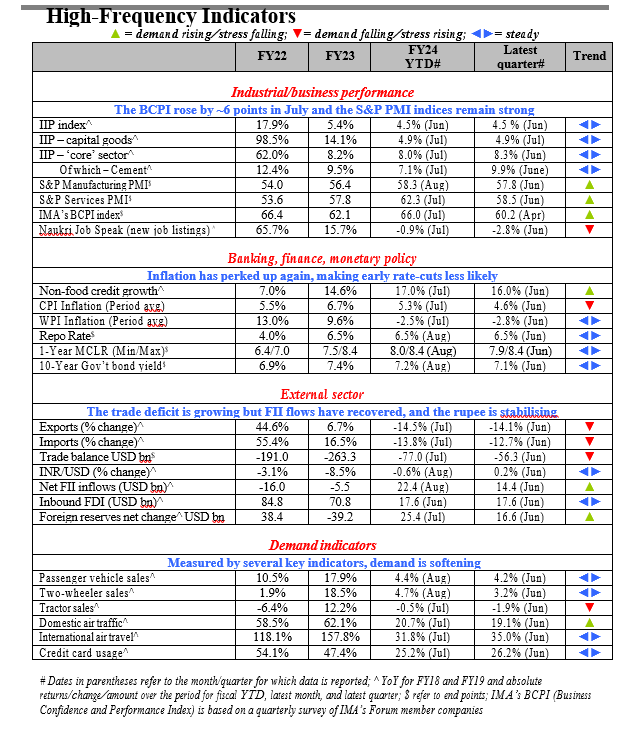

The lead macroeconomic indicators stayed buoyant through August, indicating that Q2 growth is unlikely to be much lower than Q1’s. Monthly GST receipts have stayed above the Rs 1.5 trillion mark, recording an all-time high of Rs

1.87 trillion in April. August saw a small month-on-month dip, to Rs 1.59 trillion, but this is likely to reverse in September, given that e-Way bill issuances set a new record of 93.4 million. Non-food credit growth stands at a vigorous 19.8%, led by credit to the services sector (up 23.1%). (On the other hand, lending to the manufacturing sector is growing at just 5.8%.) The S&P Purchasing Managers Index (PMI) for manufacturing remains sturdy – 58.6 in August, 57.7 in July – while the services is holding at some of its highest levels since 2010 (62.3 in July, 60.3 in August). Meanwhile, IMA’s quarterly BCPI (Business Confidence and Performance Index) suggests a strong recovery in sentiment in Q2 (Jul-Sep), with the headline index rising 6 points in July. Finally, automotive sales – a key marker of demand – continued to grow at a fair clip in Apr-Aug. Overall sales rose by 5.2%, led by commercial vehicles (14.2%), with 2-wheelers (4.7%) and passenger vehicles (4.4%) growing more

slowly. August saw a minor dip but the industry expects a volume-growth

recovery in H2 on account of the festive season and an expected (mild) recovery in exports.

Investment also appears to be picking up

Capex, including in the private sector, also appears to be on the cusp of a meaningful revival. In Q1, gross fixed capital formation (GFCF) was 34.7% of GDP, up from 31-32% in previous quarters. Further, the RBI’s latest quarterly OBICUS survey (Q4 FY23) recorded an uptick in the economy-wide capacity utilisation rate, to 75.3%, from 72.4% the previous quarter. Typically, private- sector capex tends to kick in when this rate exceeds 80%. Moreover, our BCPI survey points to sustained bullishness in the capex outlook of IMA’s member companies, with 73% (up from 70% in Q1) of businesses planning to make investments in Q2.

Indicators and forecasts at a glance

| | FY21 | FY22 | FY23 | FY24* |

Economic growth (%, 2011-12 prices) |

GDP | -5.8 | 9.1 | 7.2 | 6.0-6.5 |

Agriculture^ | 4.1 | 3.5 | 4.0 | 2.8-3.2 |

Manufacturing^ | 2.9 | 11.1 | 1.3 | 4.5-5.0 |

Services ^ | -8.2 | 8.8 | 9.5 | 7.0-8.0 |

Inflation |

CPI (%, average) | 6.2 | 5.5 | 6.7 | 5.0-5.5 |

WPI (%, average) | 1.3 | 13.0 | 9.6 | 3.5-4.0 |

Public finance |

Government borrowings, Rs tr | 18.2 | 15.8 | 14.2 | 17.9** |

Receipts net of borrowings, Rs tr | 16.9 | 22.1 | 27.6 | 27.2** |

Expenditure, Rs tr | 35.1 | 37.9 | 41.8 | 45.0** |

Fiscal deficit (% of GDP) | 9.2 | 6.7 | 6.4 | 5.9** |

External sector |

INR/USD (end of period) | 73.5 | 75.8 | 82.2 | 83.0-85.0 |

Trade deficit USD bn | 161.4 | 100.1 | 263.6 | 250-270 |

Current account balance (% of GDP) | (-) 0.9 | (-) 0.9 | (-) 2.0 | (-) 1.5-1.8 |

*IMA India forecasts unless otherwise indicated; **Government estimates; ^ GVA at basic prices (2011-12 base)

Source: CSO, RBI, DGCI&S, Ministry of Finance and CEIC

But consumption remains a concern

On the other hand, consumption, both private and public, remains constrained. In Q1, government final consumption expenditure (GFCE) dropped to 10.1% of GDP, down 0.9 pp over the year-ago quarter, while private final consumption expenditure fell by 1 pp, to 57.3%. Partly, the slowdown in GFCE may reflect the government’s focus on capital spending (a planned Rs 10 trillion this year) – and moreover, with elections due in a few months, its current spending is likely to revive shortly. However, there are signs everywhere of a multi-track consumption story. In particular, urban markets appear to be severely outpacing rural ones. Data from Nielsen indicate that Q1 was the best quarter in 18 months for FMCG sales; and majors such as Unilever, HUL, Dabur and ITC reported an upward trajectory in profit. However, while urban consumption grew by 10.2% in volume terms,

in rural India, it was just 4%, with non-food rural FMCG sales rising just 1.4%. Additionally, rural consumers appear to be purchasing smaller packs and local brands, in many cases downtrading. Looking ahead, the recent pick-up in inflation will dampen discretionary spends across the board, counterbalancing some of the lift that comes with the festive season.

Inflation is picking up again…

Inflationary pressures, after easing for several months, have recently intensified again. In July, retail (CPI) inflation touched 7.4%, up from 4.9% in June, led by a spike in food prices (11.5%, from 4.6%). Wholesale price (WPI) inflation remained in the deflationary zone at (-) 1.4%, but this compares to a much bigger, 4.1% drop the previous month. Given the sub-par rainfall through August, food inflation is expected to persist in the short term, driven by rising prices of vegetables, cereals and pulses. Since food comprises 40% of the CPI basket, this will keep the headline rates elevated. Equally, a bi-monthly survey by the RBI found that in August, the average household pegged current inflation at 8.9% (up 10bps from the June survey) and the 3-month-ahead rate at 10%. Meanwhile, crude oil prices have firmed up: the average price of an imported ‘basket’ of crude stands at ~USD 91/bbl, up from USD 74/bbl in May. Discounted Russian crude makes up ~40% of India’s oil imports, keeping prices down in relative terms, but with Russian oil exports hitting an 11-month low, this price advantage for India may go away. As far as inflation is concerned, the one ‘positive’ today is China’s economic slowdown, which is causing commodity prices in general to moderate. (The World Bank estimates that commodity prices will fall by 21% in 2023 and remain mostly stable in 2024.) All considered, the RBI has raised its CPI inflation target for FY24 from 5.1% to 5.4%. Going ahead, this probably rules out any rates cuts in the near term.

…and the external environment remains weak

Finally, the external environment remains a cause for concern. The outlook for both global GDP and trade growth this year is subdued, though 2024 may be marginally better. (The IMF pegs global growth at 2.8% in 2023 and 3% in 2024, while the WTO expects merchandise trade growth to slow from 2.7% last year to 1.7% in 2023 but to rise to 3.2% in 2024.) The causal factors include geopolitical tensions, food insecurity in various pockets, financial instability due to monetary tightening and rising public debt. Over Apr-Jul, Indian exports and imports shrank by 33% and 23%, respectively. The overall current account deficit (CAD) is expected to be in the 1.5-1.8% of GDP range, down slightly from last year’s 2% but still high. Partly counter-balancing this, capital flows – primarily on the portfolio-investment side – remain strong. FII inflows in the first 5 months of FY24 stood at USD 22.4 billion compared to USD 7 billion of outflows at the same time last year. This, and the apparent pause in the US Federal Reserve’s rate-hike cycle, has helped stabilise the rupee at 82/USD levels, for now.

-

-

-